AppsFlyer, the global leader in marketing measurement, attribution, and data analytics, has released its annual lookback at the past year’s mobile app trends. The year saw notable growth in user acquisition ad spend and revenue, fueled by increasingly advanced monetization strategies and the expanded use of AI in marketing. The findings reflect the industry’s increasing understanding of how to adapt to the ongoing changes in the market.

A decisive boost for the non-gaming space was an unmissable trend for 2024. In-app purchases (IAPs) grew nearly 20% outside gaming, driven by sophisticated monetization strategies but also inflation-related price increases. Non-gaming ad spend also experienced an increase, rising 8%, in contrast with a 7% decline in gaming categories. Within this trend Finance apps led with a significant 61% year-over-year (YoY) increase, driven by developments including growth in Crypto and FinTech, while Travel ad spend rose 20%. Shopping ad spend saw a modest decline of 8%, reflecting normalization after a 2023 surge driven by large Asian players’ aggressive worldwide market penetration.

The Middle East in particular was identified as a high-growth market in AppsFlyer’s latest report. The UAE, Saudi Arabia, Qatar and Egypt were among the countries in the region that saw an over 30% surge in mobile app installs for non-gaming categories, especially impressive when compared to the 7% global average. Marketing efforts no doubt played a significant role in driving this impressive outcome as mobile marketers across industry verticals doubled down on their audience expansion campaigns. Most notably, Finance and Generative AI app marketers in the region increased their YoY user acquisition (UA) ad spend by 208% and 94% respectively.

“The especially significant increase in UA spending in these categories indicates stiff competition and the potential for many players to continue growing their market share by appreciable levels,” said Paul Wright, General Manager Western Europe and MENAT at AppsFlyer.

Interestingly, regional shopping apps reduced their UA ad spending by 47% which might indicate a stabilization in the market, where major players have already built loyal customer bases and no longer need to rely as heavily on user acquisition campaigns. Wright stated that the pullback in spending by incumbents could make it more cost-effective and impactful for smaller players and new entrants to run successful mobile marketing campaigns.

Offering perspective on the global findings of the research, Wright said, “The data we’re seeing demonstrates not only the growth of the app economy but also the incredible creativity at play. In 2025, we expect further integration of gaming and non-gaming sectors, refined monetization strategies, and greater adoption of owned media technologies like deep linking, which will drive personalization and hybrid experiences. AppsFlyer remains committed to empowering businesses with the insights and resources they need to succeed in this dynamic environment.”

Top Data Trends of 2024

- Hybrid Monetization Drives IAA Growth: In-app advertising (IAA) revenue grew by +26% YoY in non-gaming and +7% in gaming, driven by the adoption of hybrid casual monetization strategies.

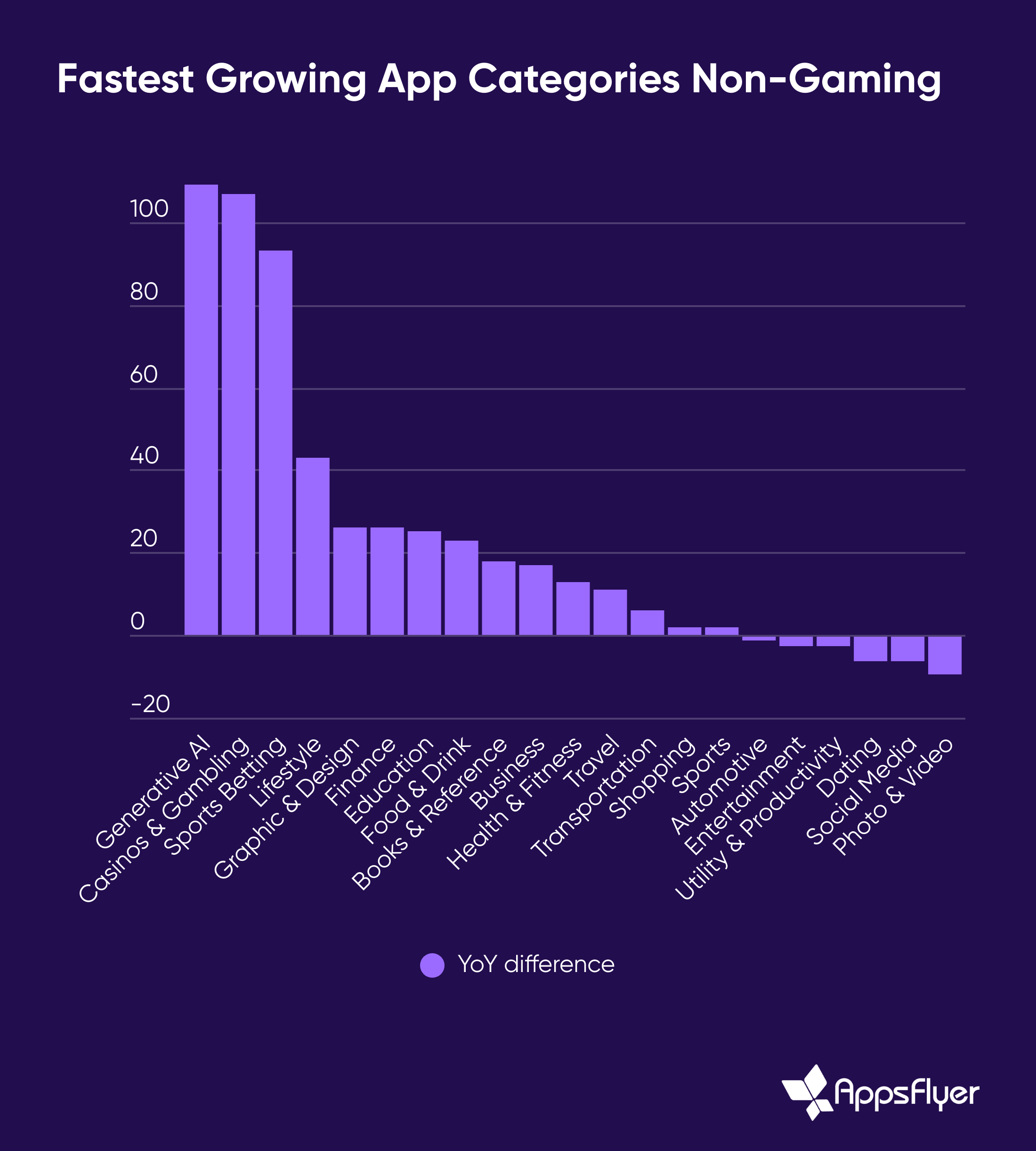

- Generative AI Dominance: Global installs grew modestly overall, with Generative AI apps achieving a standout 200% YoY increase.

- Deep Linking Expansion: Adoption surged across key channels as brands focus on owned media and maximizing lifetime value of existing users: Web-to-app led with 79% growth followed by email-to-app (+45%), text-to-app (+29%), and QR-to-app (+16%).

- Remarketing Outpaces Paid Installs: Similar to the owned media trend,paid installs grew by 22% YoY, far exceeding the 2% growth in user acquisition.

- AI-Driven Creative Innovation: The number of creative variations produced by the average app increased by 40% in 2024 to reach no less than 839 per month, driven largely by apps with larger budgets. Measuring creative performance has become an essential feature to deal with the sheer scale of creatives that have to be produced to achieve success; and that will continue through 2025.

- Leisure Categories Surge: Installs of leisure apps like Casinos & Gambling (+102%), Sports Betting (+93%) and Lifestyle (+43%) boomed, while “needs-based” app categories such as Transportation and Utility remained stable.

- Cross-Vertical Investments: Major gaming ad networks recorded a 38% YoY increase from non-gaming investments in gaming inventories, contrasting with a 19% decline in gaming investments within the gaming market. This trend is expected to continue in 2025 with more growth opportunities in non-gaming, although gaming app spend will still dominate investment in the gaming sector.

- Gaming-Specific Shifts: Casual games saw a modest 3% growth in ad spend, consolidating their market share at 64%. Hypercasual games remained stable (-1%), while Mid-core categories and Casino games faced steep declines of 21% and 12%, respectively.